🏦 Redefining Ownership

Since transaction fees are a race to the bottom…a new wave of fintechs are focused on helping you own or sell just about anything

This post was inspired by the book House of Debt by Amir Sufi and Atif Mian.

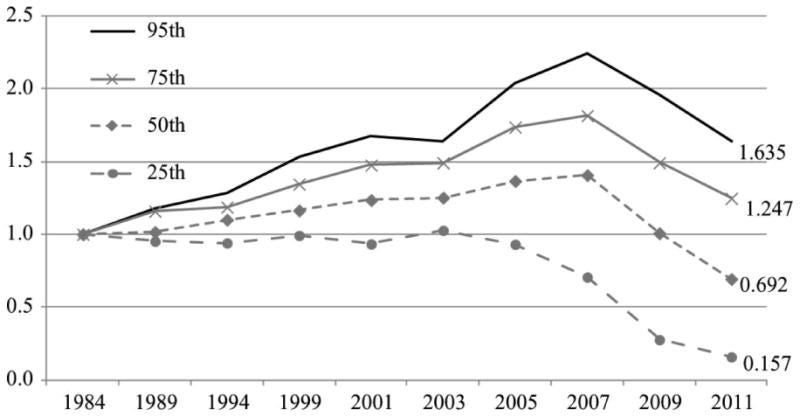

Debt is an ever present force in our lives, a driving factor that powers various aspects of our economy. However, as we navigate this intricate web of financial transactions, it becomes evident that the repercussions of debt are not evenly distributed. The levered-losses framework sheds light on how debt can intensify the impact of declining asset prices, disproportionately affecting those with the lowest net worth.

The aftermath of the 2008 recession serves as a stark illustration of this phenomenon. The surge in household debt, particularly among lower-income Americans, exacerbated wealth inequality. A prime example of the domino effect lies in the housing market, where a homeowner's equity can swiftly vanish when the value of their property plummets. In this scenario, as exemplified by the Great Financial Crisis, the lowest net-worth individuals found themselves bearing the brunt of the economic downturn.

Total net-worth by percentile relative to 1984. NLM

Against this backdrop, a new wave of fintech startups is emerging, aiming to revolutionize the way we perceive and interact with assets. These companies are pioneering fractional ownership and equity financing, ushering in a realm where the average consumer can unlock the value of traditionally illiquid assets. Beyond the crypto dimension (which I don’t plan to get into here), these innovations offer a tangible solution to the challenges posed by concentrated losses among the most economically vulnerable. I am not saying this is without risks, for what it's worth.

Fractional ownership examples:

Home equity investments: homeowners can sell a portion of their equity position in their home to an institution, creating liquidity for themselves. This functions like a preferred equity position on a physical asset. The bank is still first in line for any repayment, followed by the preferred equity investor, followed by the homeowner. This is being made possible today by companies like Hometap and Unlock.

Commercial real estate: Roofstock and Fundrise among others popularized this category nearly a decade ago and have gained serious traction. The purpose of these platforms is to help unlock broad retail access to illiquid real estate assets with high barriers to entry.

Art: Masterworks has made it possible to buy stakes in the world’s most valuable pieces of art. They directly purchase the art, store it and then facilitate the sale on behalf of all of the owners.

Other: companies like Fraction and Yieldstreet are trying to make it so anyone can invest in or sell a piece of anything. From transportation to private credit to random physical assets. I think the crypto world calls these RWAs (real world assets).

Embracing these innovative financial models underscores the remarkable creativity inherent in human efforts to shape financial products. Although fractional ownership may initially seem novel, it aligns with the enduring human tradition of crafting inventive financial instruments—ranging from bundled mortgages to complex derivatives. In this evolving landscape, the potential for a more inclusive and equitable financial future looms large, propelled by the transformative power of technology and financial ingenuity. This shift may pave the way for a truly free market, where individual influence surpasses institutional dominance.

The increasing availability of equity financing options signifies a positive evolution in finance. Models like fractional ownership democratize investment opportunities, fostering a more inclusive approach to asset ownership. Beyond portfolio diversification, this trend actively addresses historical wealth disparities, providing individuals, irrespective of net worth, with opportunities for financial empowerment. The move toward equity financing not only fortifies economic resilience but also serves as a testament to human adaptability, steering us toward a future where financial opportunities are more accessible, and wealth creation is more widely shared.

I do not know how far off this future is, but the possibility excites me. If you’re interested in similar concepts, please reach out!